Ebooks and audiobooks grow more than Print books in the Spanish Markets

By Alejandra Segovia Sánchez and Javier Celaya from Dosdoce.com

Executive Summary

- Bookwire and Libranda Annual Reports indicate that digital content in the Spanish-language markets (Latin America, Spain and U.S. Hispanic market) enjoy very healthy growth rates, between 5.7% and 4% respectively in the case of revenues from the sale of ebooks; and between 52.81% and 50% respectively in the case of audiobooks.

- Such figures outstrip Print book sales, which has only grown by 1.1% in 2022 compared to 2021, according to the report by the Federation of Publishers’ Guilds and GFK

- Unit sales continue to be the preponderant business model in the ebook market, representing an average of 75% of total turnover.

- Subscription platforms account for ⅔ of total audiobook sales in Spanish-language markets.

- Digital lending in libraries stands out very positively representing an average of 8% of total digital sales.

- Per territories, the United States recorded one of the highest growth rates in sales (+30%).

- Retail prices of ebooks have increased 8% albeit the reduction of VAT from 21% to 4%.

- 60% of ebooks sold in Spain are priced at more than 8 euros.

The sale of ebooks and audiobooks in Spanish-language markets (Latin America, Spain and U.S. Hispanic market) is in excellent health.

Madrid, June 5th. The two main distribution platforms in the Spanish Markets, Bookwire and Libranda, have published their respective annual reports on the evolution of the Spanish digital market throughout the year 2022. Both reports indicate that digital content in the Spanish Markets enjoy very healthy growth rates, between 5.7% and 4% in the case of revenues from the sale of ebooks; and between 52.81% and 50% in the case of audiobooks. Such figures outstrip print book sales, which has only grown by 1.1% in 2022 compared to 2021, according to the report by the Federation of Publishers’ Guilds and GFK.

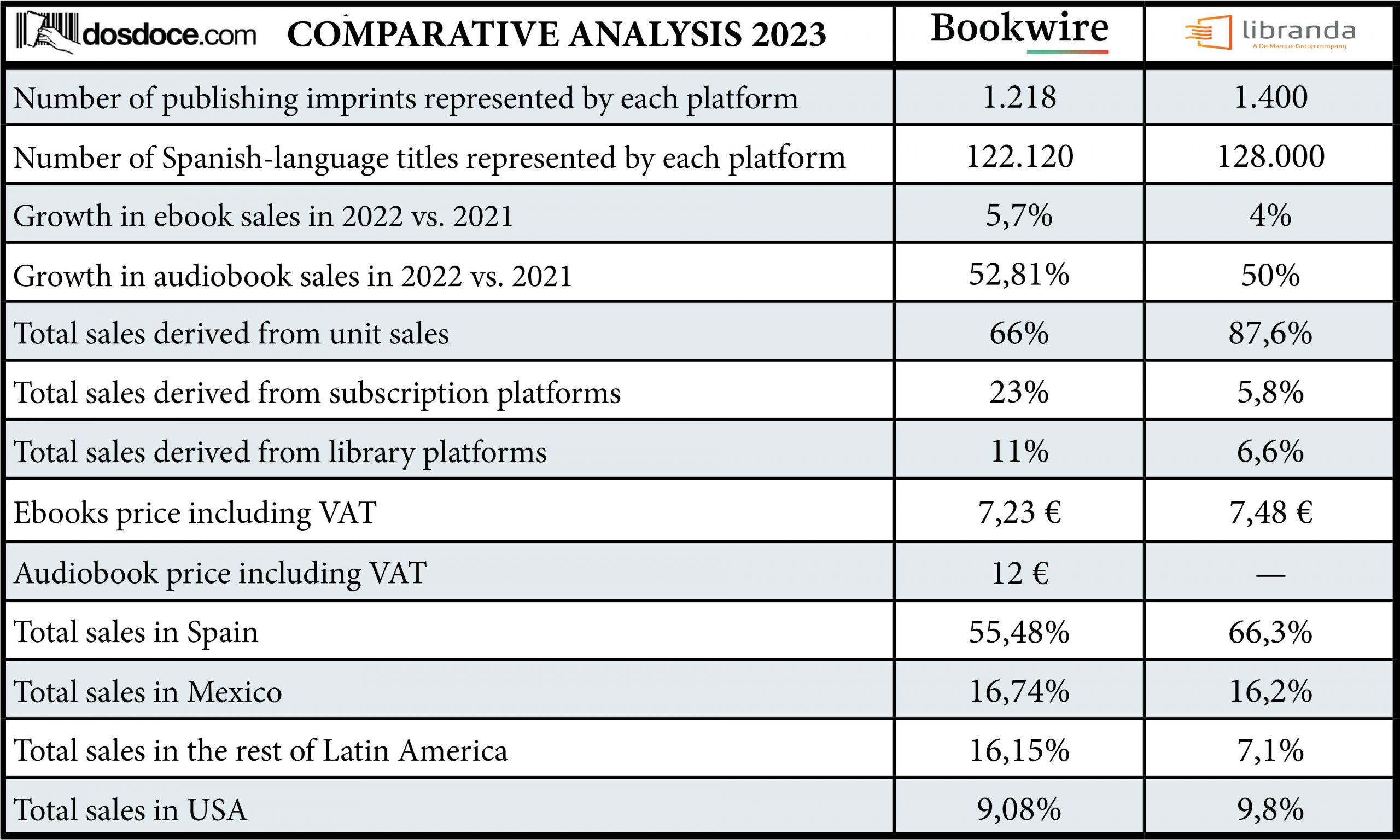

The evolution of the Bookwire platform has been spectacular over the past three years in the Spanish-language markets. In 2019 Bookwire’s catalog barely represented 45,000 titles, but by the end of 2022 it managed to almost triple, distributing more than 122,000 and aiming to close this 2023 with more than 140,000 titles belonging to 1,200 publishing imprints in the Spanish-language markets. Libranda, on the other hand, has closed 2022 with another 128,000 titles in its catalog belonging to 1,400 publishers, compared to the 90,000 titles it had in 2019. In this context of parallel growth, both platforms split the market 50/50 in number of publishers and titles, so it is highly recommended to read in detail each report separately to have a complete view of the evolution of the digital market in the Spanish-language markets.

Executive Summary Table of the Bookwire and Libranda 2023 reports.

Source: Prepared by Dosdoce.com based on data from both reports.

As in previous years, Dosdoce’s comparative analysis of both reports aims to help publishing professionals better understand the digital evolution of the Spanish-language markets. To do so, we take a closer look at the unique features of each report, as these are what make their growth different. We find the key singularities that differentiate them in the composition and focus of the catalogs they represent, in the different business development strategies implemented in the different markets (Latin America, Spain and the U.S. Hispanic market), as well as in the different commercial and distribution policies of their publishers. In addition, the methodologies of each report are somewhat different: both Bookwire and Libranda are based on actual sales incurred on their platforms, but Libranda adds an estimate valuation of the rest of the industry in their report. Regardless of these quirks and caveats, reading this comparative analysis will allow readers to get an overall look at the market and better understand the differences in respective growth.

Ebook sales continue to grow steadily

Following the unexpected growth incurred in 2020 because of changes in habits and customs forced by COVID confinements, there was concern about a slowdown in digital sales in Spanish publishing sector. However, as has been the trend in after COVID years, the figures show the opposite. As in the previous three years, both platforms report excellent growth in their respective digital ebook sales. Bookwire indicates a 5.7% growth in sales in 2022 compared to the previous year. On the other hand, Libranda has achieved 4% growth in 2022 compared to 2021.

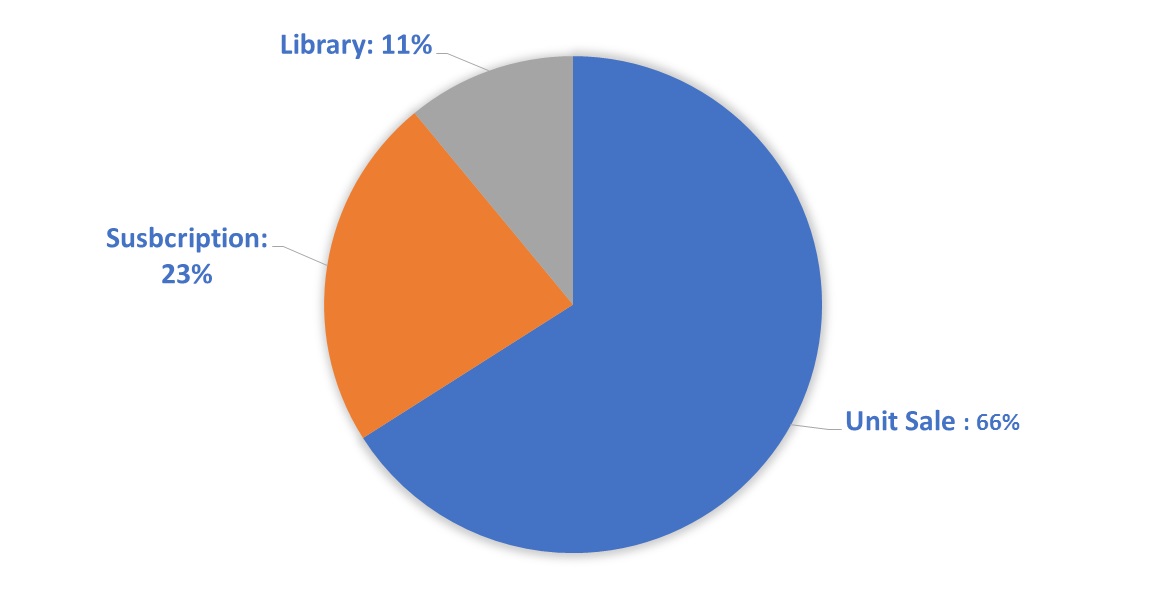

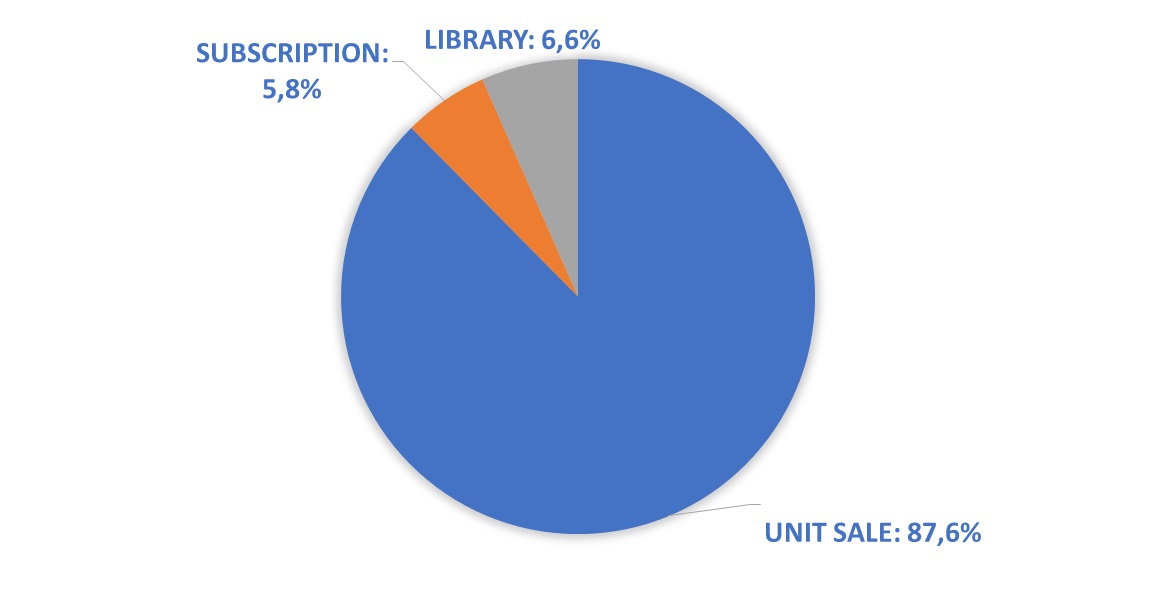

According to Bookwire’s data, unit sales continue to be the preponderant business model in the ebook market, representing 66% of total turnover, while Libranda’s report indicates that unit sales channels are also the business model with the most weight for them, coming to represent 87.6% of total ebook sales in Spanish-language markets.

Given the relevance of this channel in both platforms, it is interesting to break down the data for this model to better understand its behavior. The greatest weight of the market falls once again on international platforms (Amazon, Google, Kobo, etc.) with a share of 75.3%, which represents. On the other hand, independent bookstore chains, bookstores and online platforms experience a growth of 31% and their share reaches 12.3% of the market in 2022.

Subscription platforms represent 23% of Bookwire’s total sales, while for Libranda they represent 5.8%.

One of the most interesting aspects that emerges from the comparative analysis of the Bookwire and Libranda reports is the different evolution that the subscription business model is having in each of them due to the business policies of the publishers they represent.

The subscription model for the publishers that Bookwire represents continues to increase its prominence, billing 23% of the total sales, which implies a growth of one point compared to the previous year. It is worth noting that Spain led the growth in this sales model, with 27.8% over last year.

Graph 2. Breakdown of Bookwire platform sales channels.

Source: Dosdoce.com based on data from Bookwire Report

According to the Libranda report, e-book subscription platforms has experienced a significant decrease for the first time with respect to the previous year (-15%), reducing their share to 5.8% of total sales in 2022.

Graph 3. Breakdown of Libranda platform sales channels.

Source: Dosdoce.com based on data from Libranda Report

What is the rationale behind the difference in subscription channels performance between Bookwire and Libranda data?

It is not something new, it has been repeated for years in the annual reports, nor is it because one platform is doing better than the other. In our view, the different growth rates of Libranda and Bookwire in subscription channels stem from the nature of the publishers they represent and their commercial policies. Several publishers apply commercial restrictions on the different subscription and streaming platforms limiting their growth potential in one of the most rapidly expanding channels in the Spanish Markets in the recent years.

Whereas most of the titles distributed by Bookwire, which represent 50% of the market and are part of large publishing groups (Grupo Planeta, HarperCollins, Grupo SM, Grupo Océano, among others), are marketed in all sales channels (unitary download, subscription platforms and digital lending in libraries) with almost no restrictions. This means that publishers benefit from more revenue by selling all their titles by applying a multi-distribution strategy across all sales channels.

Subscription platforms account for ⅔ of audiobook sales in Spanish-language markets.

Due to its rapid growth in the last 5 years, the audiobook category has come to have a section in each of the reports we are analyzing. However, although Bookwire devotes a fairly extensive section to this part of its analysis, Libranda does not provide enough data to carry out a comparison similar to the one we have done in the ebook section, but fortunately there are other complementary studies that allow us to analyze the evolution of this category in the Spanish-language markets. What we can confirm is that both Bookwire and Libranda have seen a rather striking growth compared to the previous year, 52.81% and 50% respectively.

According to the Bookwire report, subscription platforms are the main sales channel for audiobooks, accounting for 73.69% of total sales. In second place, and a long way behind, is unit sales, a model that accounts for 20.01% of the total market. Finally, 6.3% of the sector’s turnover comes from the consumption of audiobooks in public libraries.

The consumption of audiobooks in Spanish is divided into three large territorial blocks. On the one hand, more than a third of the turnover of these audio catalogs comes from listening in Spain: 38.07%. A very similar percentage, 39.42% of revenue comes from listening generated in Mexico (27.78%) and Latin America (11.64%). Finally, listeners in the United States accounted for 22.52% of the total. In this regard, the constant growth of interest in the United States in Spanish-language culture is noteworthy, since in 2022 the consumption of audiobooks increased by 82.94%. Unlike ebooks, which have experienced an 8% increase in their RRP in 2022, the average RRP of audiobooks is 12 euros, a very similar price compared to 2021.

On the other hand, the first Map of the Spanish Audio Industry recently published by Dosdoce.com has detected more than 430 entities that have strongly bet on the development of the new audio industry in the Spanish markets (Latin America, Spain and the US Hispanic market) during the last five years. During this time, these entities have created more than 100,000 podcasts and nearly 25,000 audiobooks in Spanish, among other audio formats, compared to the scarce Spanish-language audio content of just a few years ago. An industry that is expected to grow to 26.6 million listeners in 2026 and that these will grow up to 30% year-on-year and generate revenues of 590 million euros through advertising, branded content, subscription revenues, unit sales, etc., according to a study by PwC.

Digital lending in libraries is growing steadily

As we can see, in both platforms there has also been a very significant growth in digital lending projects through public libraries, institutional libraries, school libraries and private or corporate libraries.

According to the Libranda report, the category of digital lending in libraries stands out very positively, with 33% growth over the previous year and representing 6.6% of total sales. According to the Bookwire report, the revenue generated by digital platforms for libraries will also grow healthily in 2022 to reach 11% (three points more compared to last year). According to Bookwire, Spain accounted for 46% of the revenue generated by this business model, followed by Latin America, with 28%. The United States has established itself as the third most important territory in terms of library revenues, with 19% of the total, and Mexico accounted for 5% of the total.

The broad growth in the area of libraries indicated by both platforms is due to the great investment effort made this year in the acquisition of new funds by different institutions. Particular mention should be made of the plan that the Ministry of Culture and Sport has implemented with the support of the EU Next Generation Funds, as it has made it possible to establish this channel as a stable source of income. The eBiblio project is the most significant, although there are many others, such as the electronic library of the Cervantes Institute, the eLiburutegia platform of the Basque Government, eLibro, Odilo, among others.

The United States recorded one of the highest growth rates in sales (+30%).

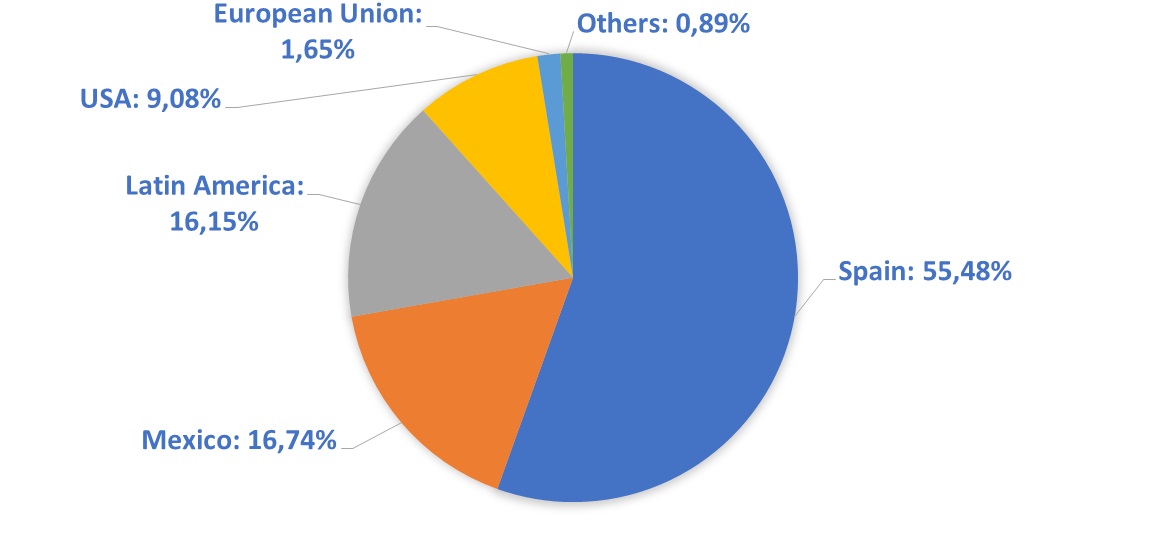

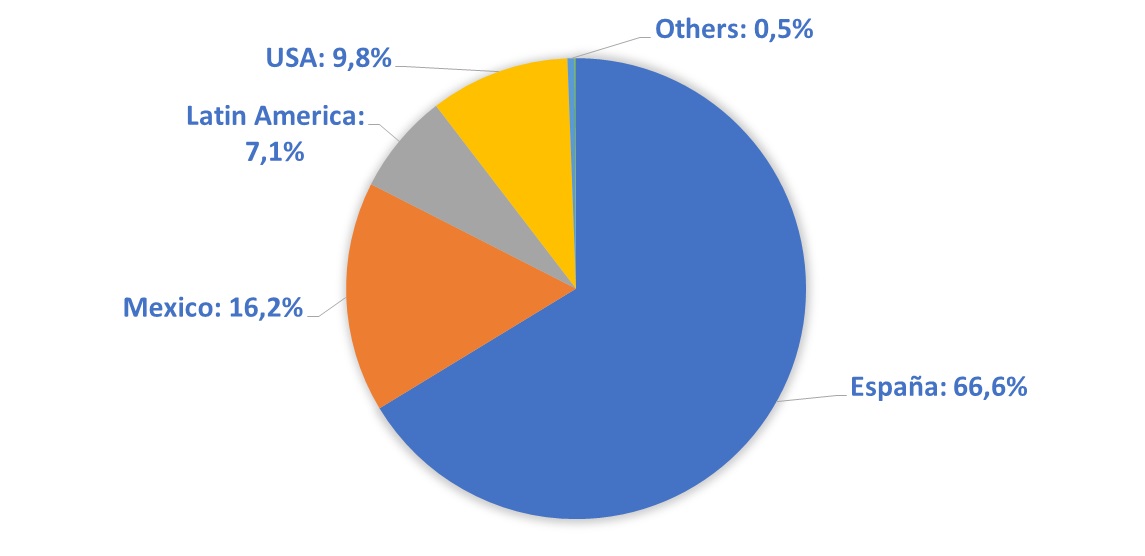

Another very interesting aspect that we can highlight from the comparative analysis of these reports is the different evolution of sales according to territorial distribution. For both Bookwire and Libranda, Spain continues to be the country with the highest digital sales, with 55.48% and 66.3% respectively.

Sales in Mexico according to Bookwire are 16.74%, which is fairly equal to Libranda’s results of 16.2%. We also find similar results in the USA, where Bookwire accounts for 9.08% of the total compared to 9.8% for Libranda, although in the case of Bookwire, the increase in turnover in the US stands out, reaching 32.12% compared to the previous year.

The biggest differences can be seen in the rest of the Latin American market (Argentina, Colombia, Chile, Peru, etc.), where Bookwire accounts for 16.15% of total sales, compared to 7.1% for Libranda.

Graph 4. Breakdown of Bookwire’s sales by territory.

Source: Own elaboration based Bookwire Report (2023).

Figure 5. Breakdown of Libranda’s sales by territory.

Source: Own elaboration based on Libranda Report (2023).

Source: Own elaboration based on Libranda Report (2023).

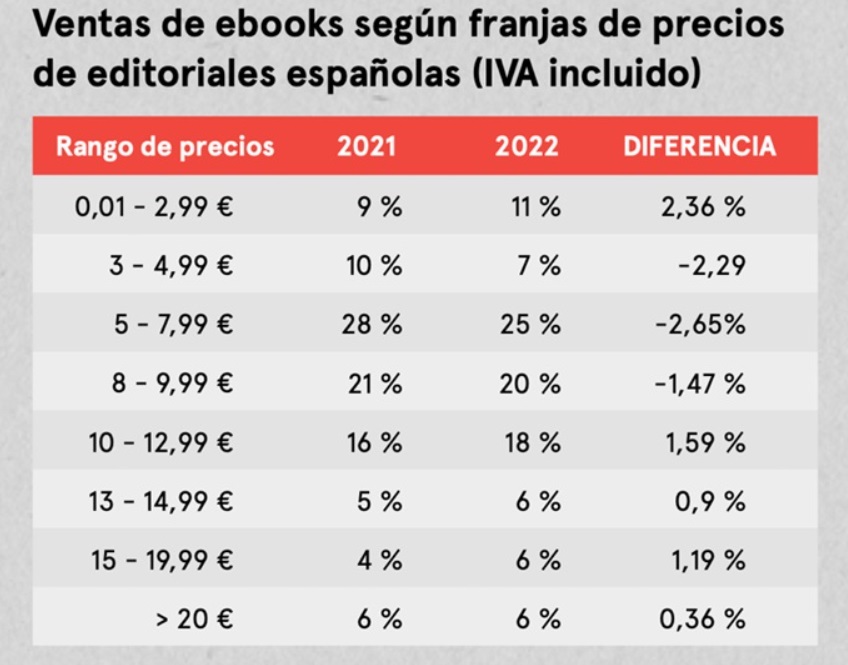

60% of ebooks sold in Spain are priced at more than 8 euros.

Although in 2020 the government of Spain announced the approval of the lowering of VAT on ebooks from 21% to 4%, unfortunately retail prices have increased to 8% in 2022 compared to 2021. Specifically, in Spain the average retail price has risen from €7.07 to €7.48 (VAT included), according to Libranda, and from €6.70 to €7.23 (VAT included) according to the Bookwire report. In this context of the price scale, 60% of ebooks sold in Spain are already priced at over 8 euros.

If we analyze the evolution of the publishers located in Spain according to the data provided by Bookwire, the RRP with the highest market share is between 5 and 7.99 euros, which represents 25% of the total, with a decline of three points compared to the previous year. It is followed by the segment between €8 and €9.99 with 20%, down one point compared to 2021. In third place are the prices between €10 and €12.99, which account for 18% of the total, up two points. In fourth place, prices up to 2.99 euros, with 11% of the total and a growth of two points. 3 to 4.99, with 7%, a decrease of 3 points. Finally, the groups between 13 and 14.99 euros, 15 and 19.99 euros and more than 20 euros each accounted for 6%.

Figure 6. Sales of ebooks by price range

Source: Bookwire Report (2023).

Source: Bookwire Report (2023).

Links to the reports mentioned in the comparative analysis: